TL;DR

- Accenture judges the traditional media industry as facing “dire circumstances” and says modest strategic adjustments and limited initiatives won’t work.

- Traditional media companies must reinvent themselves systemically, from the ground up, making moves such as merging with a video game company.

- This reinvention includes a fresh look at target audiences, an openness to competing in new industries, and a willingness to admit limitations in existing skillsets.

READ MORE: Reinvent for growth: Only the radical survive (Accenture)

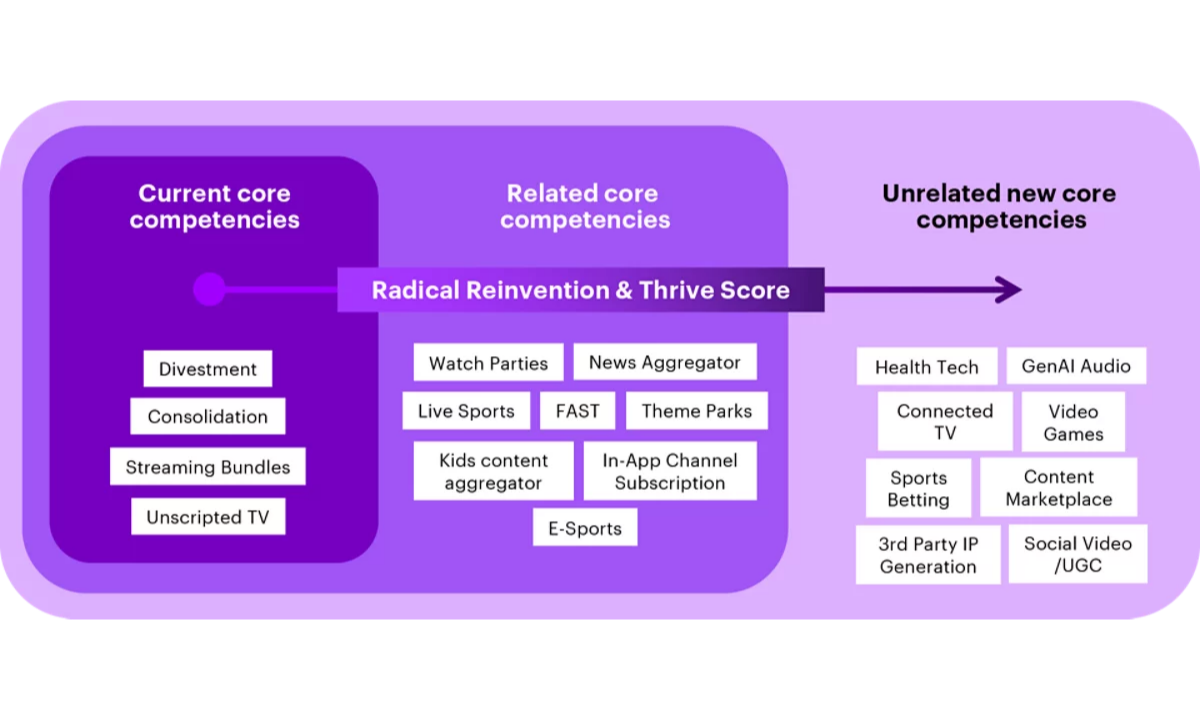

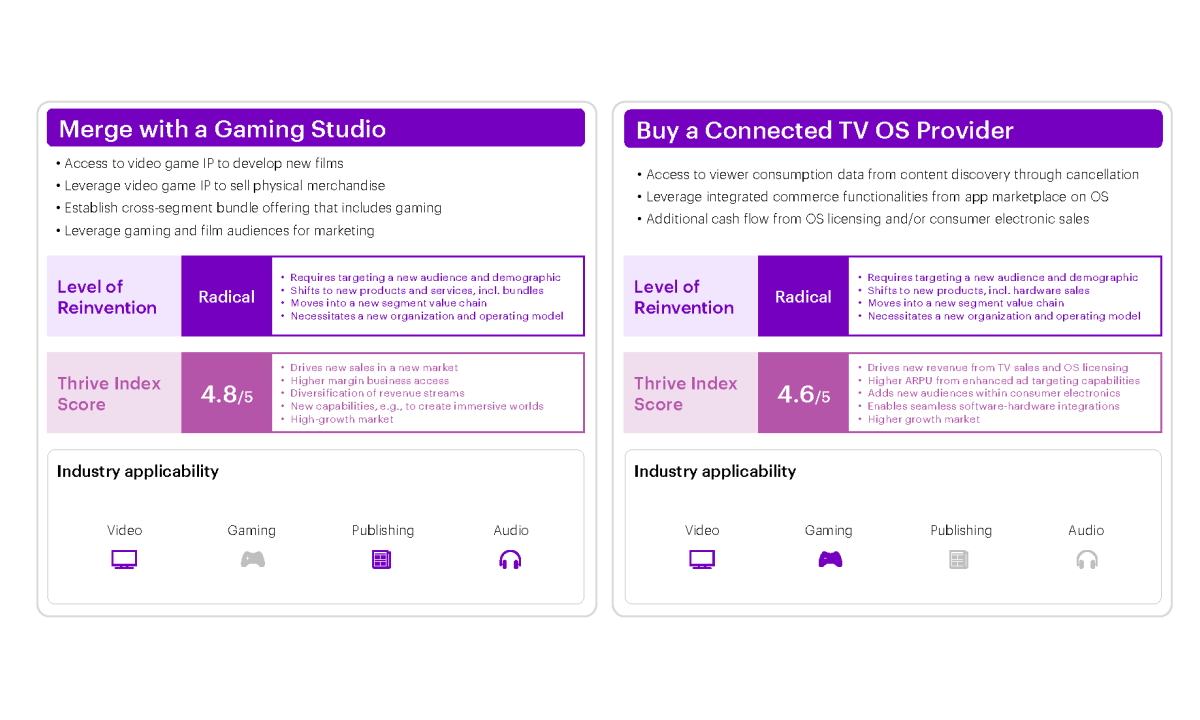

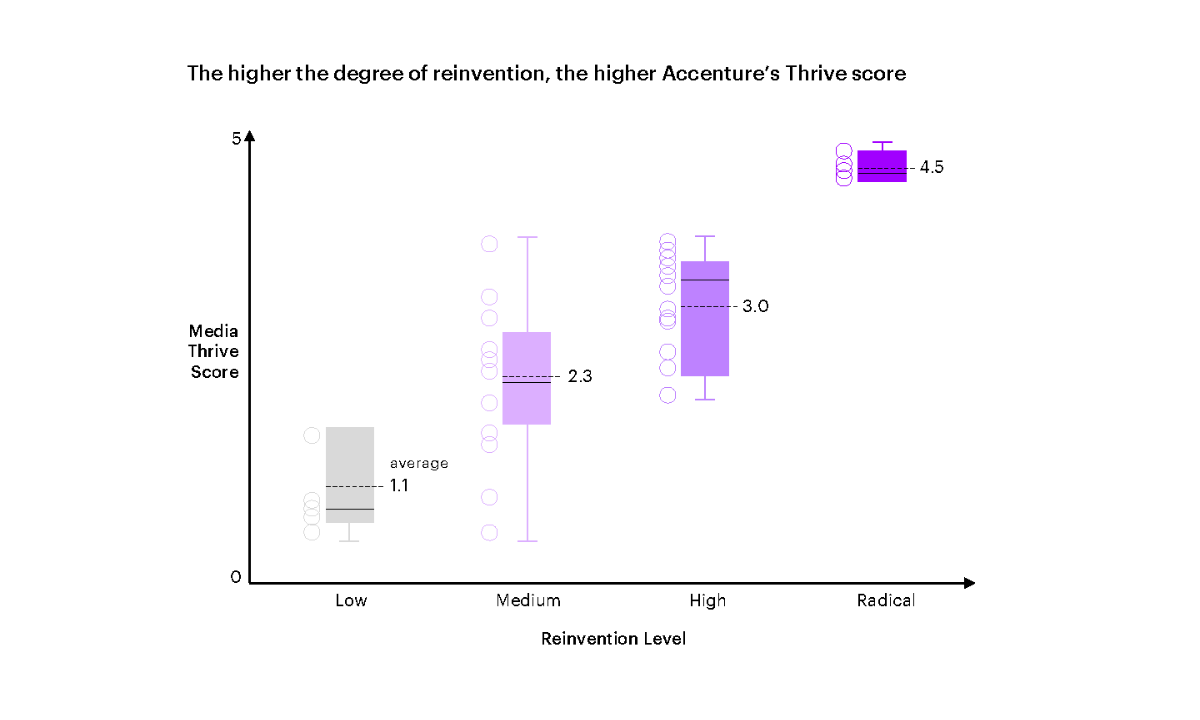

Click here for a larger version of this graphic.

Merging with a video game studio and/or acquiring a Connected TV operating system provider are some of the radical “big bets” that legacy media companies must place if they are to survive, according to industry consultants Accenture.

“Traditional media companies must reinvent themselves from the ground up,” urge Accenture execs Swati Vyas, senior principal of global communications & media research lead, and Greg Merchant, managing director of strategy, the authors of the report, “Reinvent for growth: Only the radical survive.”

Getting radical means Media & Entertainment must step outside its comfort zone, “beyond current competencies,” effectively no longer being a media-first company.

The report pulls no punches. And if it scares major studios into seeking the help of Accenture’s management consultants it will have done its job.

Just to make sure, the report begins by underlining the troubled landscape facing M&E.

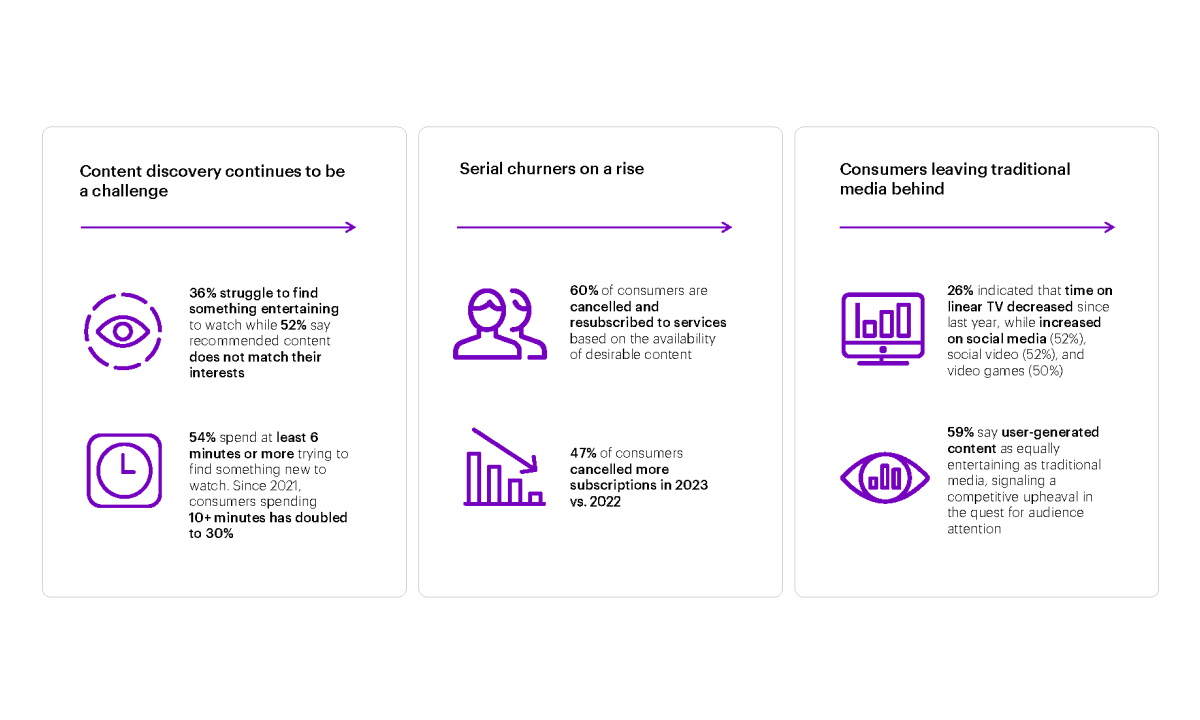

Highlighting a “seismic shift” in entertainment preferences, 59% of consumers polled in the report regard user-generated content as equally entertaining as traditional media, signaling a competitive upheaval in the quest for audience attention. Meanwhile, nearly 60% say they trust independent content creators as much as they do established news media.

While there’s “clear consumer bias” for SVOD services, growing customer dissatisfaction (about cost, inability to find content, and multiple service sign-ups) has created widespread and serial churn, which is not a solid ground on which to pitch investments.

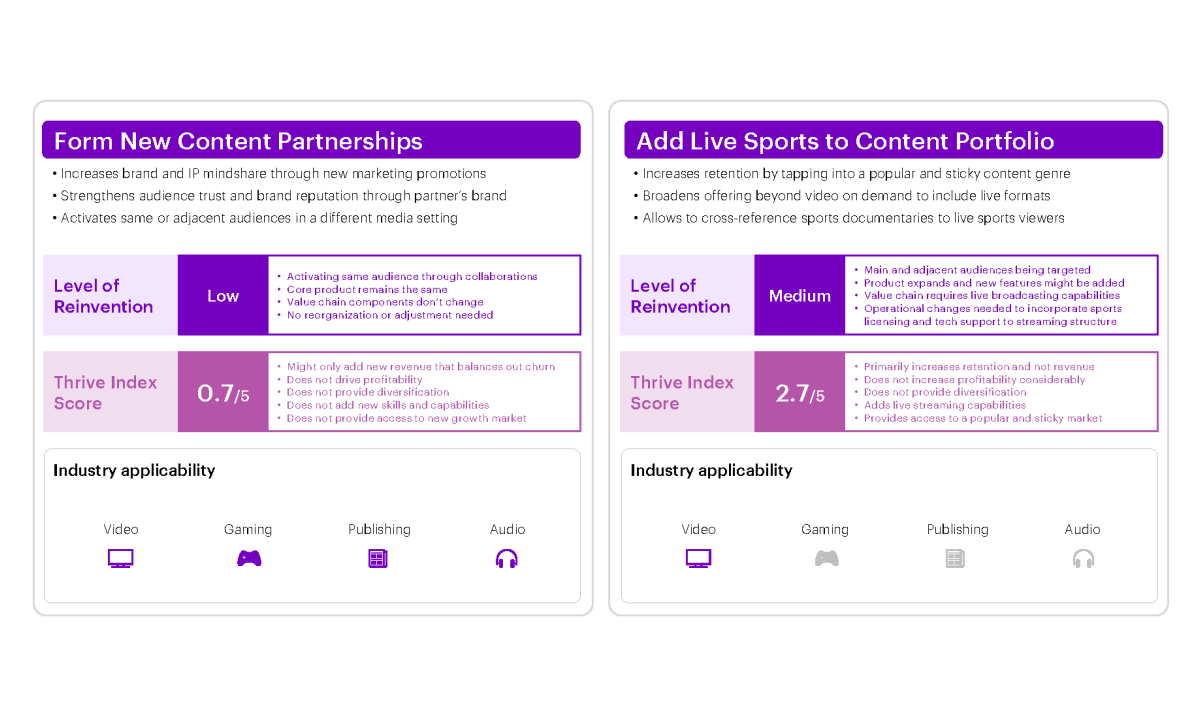

What’s more, attempts by the major studios, networks and streamers to change course by — for example, doubling down on buying live sports rights or bulking out content libraries — is just tinkering around the edges of a doomed business model, in Accenture’s view.

“Some have achieved short-term gains by doing those things, but even for them, the big picture looks bleak,” it states, adding that such strategies “will not significantly impact a media company’s economic profile or reset its revenue trajectory.”

What’s more, Big Tech casts a long shadow. Amazon, Google, Apple and Microsoft are expected to grow more than two times faster in operating cash flow than legacy media (10.6% vs. 4.8%) during 2023-25. These companies are also investing in streaming, gaming and live sports. “Their diversified revenue streams give them a safety net that pure-play media companies don’t have.”

That’s what Accenture now calls on M&E players to do.

“Legacy media companies need new sources of revenue; they need to take on new roles in the entertainment value chain. They need to rethink the customers they serve and even the industries where they chose to compete.”

Since half the consumers it surveyed report spending more time playing video games, Accenture advocates that M&E companies partner with video game developers.

Netflix’s move into mobile gaming and Disney’s acquisition of a $1.5 billion stake in Epic Games can be seen in this light.

Since 40.1% of respondents surveyed often use cross-service search engines to find content and services plus the fact that ad dollars accelerating away from linear onto digital video, the consultancy also suggests buying a CTV platform is “a compelling strategy for media companies.”

Comcast’s partnership with Charter Communications to launch Xumo, which introduced a CTV operating system integrated with streaming services, gaming and music apps and radio stations, is held up as one example.

Walmart recently entered the space through its acquisition of Smart TV maker Vizio in 2024, largely to expand its retail media business to compete with Amazon.

A potential suitor might consider CTV platform Roku, with rumors of its potential sale circulating more than a year ago.

Accenture also points to how Big Tech companies have diversified revenue streams across “consumer lifestyle services” as a model for media to follow.

It projects consumer spending on lifestyle bundles — such as grocery delivery, photo storage, video game streaming, and pharmacy assistance alongside streaming video and music — to reach $3.5 trillion by 2030.

“It’s an enormous mandate, but a tremendous opportunity,” Accenture says, highlighting that Sony Pictures and The New York Times are trying to move in this direction.

Instead of launching into streaming, Sony Pictures has focused on producing and selling content to the big streamers in addition to reinvigorating its portfolio to span video games, Accenture says; meanwhile Sony Corp. is moving into making electric vehicles.

At the same time, the Times is “gaining new strategic and financial resilience” through a portfolio that includes consumer apps for audio/podcasts, sports, cooking, shopping, and games.

It’s not clear if these are both Accenture clients.

Another example highlighted in the report is the union of Walmart and Reliance Jio in India to extend joint businesses in the region across connectivity, news, books, movies, music, payments, groceries, devices, and more.

Going down this route is not without a major challenge. Even if, say, Warner Bros. Discovery was to buy Riot Games it would still need to revamp its executive team.

“Film production efficiency, advertising sales excellence, and seamless broadcast operations aren’t enough to build on,” Accenture says. Neither are “esoteric competencies” such as “storytelling” and “franchise management” sufficient for success in “complex new areas such as video game development.”

M&E companies must venture “boldly” into areas and consumer markets “where, currently, their expertise may be limited.” For example, legacy media firms are not skilled in navigating the intricacies of social media platform management, nurturing content creator economies, or exploring the potential in sports betting, the company says.

“However, these sectors represent vital opportunities for growth and are pivotal for any company looking to flourish in the modern age.”

Why subscribe to The Angle?

Exclusive Insights: Get editorial roundups of the cutting-edge content that matters most.

Behind-the-Scenes Access: Peek behind the curtain with in-depth Q&As featuring industry experts and thought leaders.

Unparalleled Access: NAB Amplify is your digital hub for technology, trends, and insights unavailable anywhere else.

Join a community of professionals who are as passionate about the future of film, television, and digital storytelling as you are. Subscribe to The Angle today!